With the April 15, 2026 federal tax deadline now sixteen days away, the question I keep hearing from working families isn’t about deductions or credits. It’s simpler than that: when does the money actually show up? For most people, a delayed refund is an inconvenience. For Kevin Andersen, a 36-year-old union journeyman electrician from Minneapolis, a delayed refund was the difference between moving forward and staying frozen.

When I met Kevin at a coffee shop near his home in South Minneapolis earlier this month, he arrived ten minutes early carrying a small notebook. He set it on the table without opening it — he had the numbers memorized by then. His wife Mara is due with their first child in late July. He had filed his 2025 federal return on February 6th, expecting a refund of approximately $3,200. Forty-seven days later, it still hadn’t arrived.

The Financial Equation That Wouldn’t Balance

Kevin and Mara earn a combined $105,000 a year — Kevin pulls roughly $68,000 in union wages; Mara earns $37,000 as an office administrator. They are, by Kevin’s own description, disciplined people. They pack lunches. They carry no credit card balances. They started saving seriously three years ago after reading a stack of personal finance books Kevin keeps in a short shelf above his workbench. None of that changed the math they were staring at.

They had $22,000 in a high-yield savings account when Kevin filed — earning around 4.3% APY, which he tracked carefully. That sounds like meaningful progress. But Kevin had assigned every dollar of it to two different urgent destinations at the same time, and that was the problem.

A modest three-bedroom starter home in the Minneapolis metro neighborhoods they were targeting was running between $320,000 and $360,000. A 10% down payment on a $330,000 home would require $33,000. Add estimated closing costs of $6,000 to $9,000 and they needed roughly $39,000 to $42,000 before they could seriously submit an offer. They were $17,000 to $20,000 short, minimum.

The emergency fund calculation was equally sobering. Mara planned to take twelve weeks of unpaid maternity leave — approximately $10,800 in missing income over three months. Out-of-pocket hospital and newborn costs under their insurance plan were estimated at $4,000 to $7,000. Kevin wanted six months of living expenses set aside before her leave began. Their monthly baseline: roughly $5,200. Six months: $31,200. Their $22,000 covered about 70% of that.

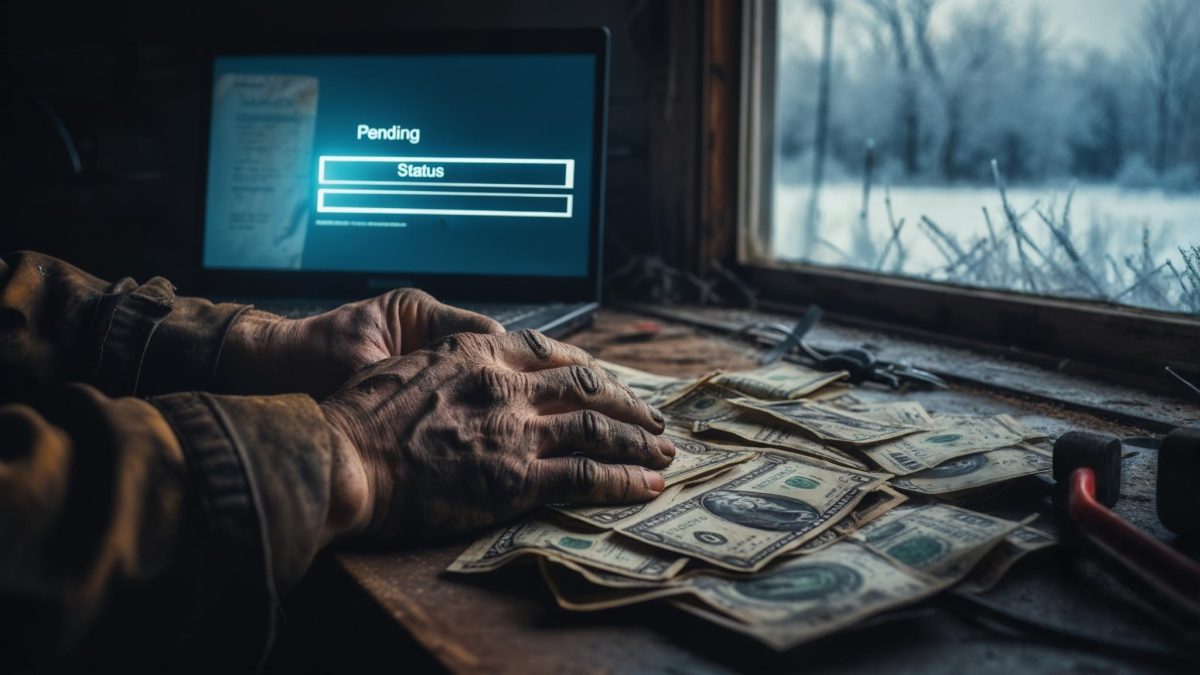

“I kept thinking the refund would at least move the needle,” he told me. “Like, even if it didn’t solve everything, $3,000 landing in the account would feel like progress. Every time I opened that IRS tool and saw ‘processing,’ something in me just deflated.”

Forty-Seven Days of Checking “Where’s My Refund”

Kevin e-filed his 2025 return on February 6th using tax software, selecting direct deposit to his savings account. His return was straightforward: two W-2s, standard deductions, no EITC, no amended items, no self-employment income. According to the IRS Where’s My Refund tool, the agency typically issues refunds within 21 days for electronically filed returns with direct deposit. Kevin had no reason to expect complications.

By day 21, the tool still showed “processing.” Kevin started checking every morning before his shift. By day 35, he had read enough Reddit threads about delayed refunds to have convinced himself, briefly, that he’d been flagged for review. He hadn’t. He received no IRS notice, no CP05 letter, no request for additional documentation.

The delay, as best Kevin could determine after the fact, was routine volume-related processing. The 2026 filing season opened January 27th, and the agency processed tens of millions of returns in the first six weeks. Some simply took longer without any adverse reason attached. “My brother-in-law filed two weeks after me and got his refund in eleven days,” Kevin said. “I don’t know what to tell you.”

Kevin described the daily ritual of checking with a mix of self-awareness and frustration. He knew, intellectually, that opening the app more often wouldn’t change the outcome. He did it anyway. “I’ve read four personal finance books in the last year,” he told me. “I know what I’m supposed to do. But knowing and doing are different things when you’re looking at your wife and thinking, what if I get this wrong?”

When the Deposit Finally Landed

On March 24th — forty-six days after Kevin filed — the status on IRS Where’s My Refund changed to “Refund Sent.” The next morning, March 25th, $3,147 appeared in his savings account. The final figure came in $53 lower than his original estimate, the result of a small IRS adjustment to his return — something Kevin told me he still hadn’t fully traced back to a specific line item.

He sent me a two-word text that morning: “It’s here.” I called him that afternoon and he picked up on the second ring.

“I felt relieved for about twenty minutes,” Kevin told me over the phone. “Then I started doing the math again, and I was right back where I started. $25,147. Still not $42,000. Still not $31,000. Just closer to nowhere fast.” He said it without bitterness. More resignation than anything else.

The Decision He Still Questions

Kevin decided — after what he described as three nights of lying awake running scenarios — to put the entire $3,147 into the emergency fund bucket. He and Mara talked it through over dinner, went back and forth, and landed on the position that with an unpaid maternity leave starting in roughly sixteen weeks, having liquid cash available mattered more than contributing to a down payment fund that was still more than $15,000 short of being usable anyway.

The house search is on hold. The Minneapolis market had already humbled him twice — he’d been outbid on two properties the year before, both times by cash buyers coming in $15,000 to $20,000 over asking price. “Cash buyers would come in and that was the end of that,” he told me flatly. Pausing the search stings, but Kevin framed it as a deliberate reset rather than a failure. Whether he fully believes that, I couldn’t say.

What I kept coming back to, after leaving that coffee shop and after our follow-up call, was how thoroughly Kevin had prepared — and how little that preparation had quieted the anxiety. He knew his numbers cold. He understood the tradeoffs between liquidity and leverage. He’d done the reading. And yet the waiting — for the refund, for the baby, for some version of clarity — hadn’t gotten easier with more information. It had just gotten more specific, and therefore harder to dismiss.

“I keep telling myself, four months from now things will be different,” he told me before we wrapped up. “And I know they will be. But I can’t tell if I mean better or just different.” He closed the notebook. Left it on the table. Went back to work.

His April 15th deadline is a formality at this point — Kevin filed months ago and the IRS has long since processed his return. The $3,147 is sitting in a savings account in South Minneapolis. The baby is still four months out. The house is still someone else’s. Some financial stories don’t resolve cleanly inside a single tax season, and Kevin Andersen’s is one of them.

Leave a Reply