Patience is not a tax strategy — and anyone who tells you otherwise has probably never needed a refund check to cover overdue property taxes. That is the hard truth Byron Quintero, 56, a licensed plumber from Albuquerque, New Mexico, landed on after one of the most stressful springs of his adult life.

I met Byron by chance in late February at the Ernie Pyle Branch Library on Copper Avenue. I was there covering a Medicare open enrollment information event when a broad-shouldered man in a faded blue Carhartt jacket sat down next to me during a break and said, almost to himself, “I filed six weeks ago and I still have nothing.” He was not talking about Medicare. He meant his tax refund.

Over the next two hours — and in two follow-up calls in March and April — Byron walked me through what became a 61-day ordeal with the IRS that tested his composure, strained his finances, and left him with a skepticism about the refund process that will take years to fade.

A Refund With a Job to Do

Byron earns roughly $94,000 a year running his own licensed plumbing operation, a one-man shop he built over two decades after a brief detour into academia. In his early 40s, following the death of his wife Carmen, he enrolled in a graduate program in construction management at the University of New Mexico, hoping to pivot into project management. He finished the degree but never made the leap — the plumbing work was steadier, and grief, he told me, changed his appetite for risk.

That degree left him with approximately $31,000 in federal student loan debt that he is still repaying at 56. Combined with property taxes on his three-bedroom home in the South Valley neighborhood that had fallen $4,800 behind after a slow stretch in 2024, Byron was carrying more financial pressure than his income alone suggested.

“I had that refund earmarked,” Byron told me, leaning forward over a library table scattered with Medicare pamphlets neither of us had touched. “Three thousand four hundred dollars was going straight to the county assessor’s office. That was the plan from January.”

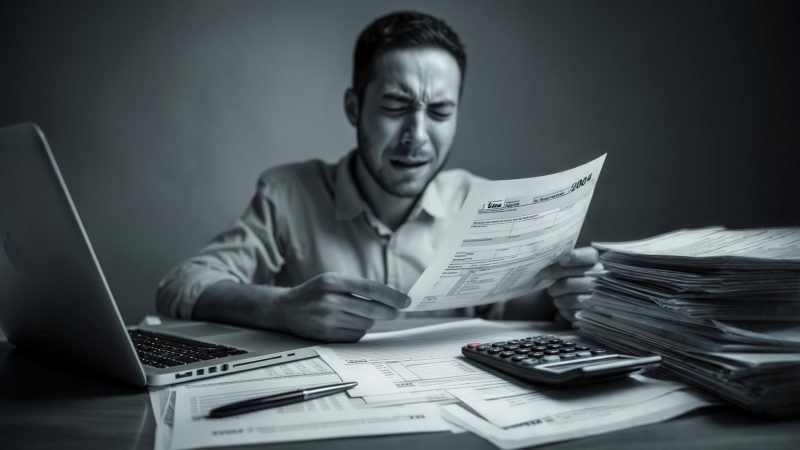

He filed his 2025 federal return electronically on February 14 — Valentine’s Day, a detail he noted with a dry laugh. He had used a tax software program he had relied on for years. His return was accepted the same day. The IRS had officially opened the 2026 filing season on January 27, according to ABC7 News, with a filing deadline of April 15 for most taxpayers. Byron was early. He had every reason to expect smooth sailing.

When “Processing” Becomes a Warning Sign

The IRS “Where’s My Refund?” tool showed Byron’s return as “Received” within 24 hours. By day five it moved to “Processing.” Then it stayed there. For weeks.

By day 28, Byron started calling the IRS helpline. He described the experience with the kind of weary precision that only comes from having done something frustrating many times. “You call, you wait, sometimes forty minutes, and then you get someone who reads back what the computer already told you,” he said. “‘Your return is being processed.’ I know it’s being processed. I want to know why it hasn’t moved.”

The IRS does advise taxpayers to wait at least 21 days after e-filing before calling, and longer if the return involves certain credits. Byron’s return included a deduction tied to his home office — a dedicated space in his garage where he handles invoicing and scheduling for his plumbing jobs. That detail, he would later learn, triggered a manual review flag.

The CP Notice That Changed Everything

On March 19 — 33 days after filing — Byron received a CP05 notice in the mail. The letter informed him that the IRS was reviewing his return to verify income, tax withholding, and certain deductions, and that it could take up to 60 additional days to complete the review. No action was required from him — yet.

“That letter dropped my stomach,” Byron said. “I read it three times thinking I had missed something. Sixty more days? My county tax payment was already 30 days late at that point.”

A CP05 notice does not mean the IRS suspects fraud. It is a routine review mechanism, more common when a return includes business-related deductions, Schedule C income, or credits that require verification. Byron had a Schedule C attached to his return for his plumbing business. The home office deduction — he estimated about $2,100 — was the likely trigger, though no IRS representative confirmed that to him directly.

The Bernalillo County Treasurer’s Office, where Byron’s property tax account sits, charges a 1% monthly penalty on delinquent balances. On a $4,800 arrearage, that meant roughly $48 per month accumulating while he waited.

The 2026 Refund Landscape Byron Was Navigating

Byron’s situation played out against a broader backdrop of confusion and misinformation about IRS refunds and payments in early 2026. Throughout the year, claims about new stimulus checks, tariff dividends, and special IRS direct deposits spread widely on social media, according to Fox5 DC’s fact-check reporting. None of those claims were accurate — there were no new stimulus checks, no tariff dividend payments, and no special IRS relief deposits beyond standard refund processing.

Byron had heard some of the stimulus rumors circulating online. He dismissed them — he had been burned before by financial misinformation and developed a healthy skepticism toward anything that sounded too good to be true. “I learned a long time ago not to plan around money that isn’t confirmed,” he said. “That’s a lesson that cost me the first time.”

He was referring to a period in 2019 when he counted on a large contract payment arriving on a specific date, used the expectation to cover a shortfall, and found himself behind when the client delayed. That experience, he said, reshaped how he handled financial timing — which made the IRS delay feel like a particular kind of betrayal. This time he had done everything right.

For context on what larger refunds might look like in coming years, CNBC reported that changes in President Trump’s 2025 legislation could push average refunds higher in the 2026–2027 cycle. Byron was not yet factoring that in. He just wanted his $3,400.

The Day the Money Finally Arrived

On April 16 — 61 days after Byron filed — his bank account showed a deposit of $3,400 from the U.S. Treasury. No advance notice on the tracker. No letter confirming resolution of the review. Just money, arriving on a Thursday morning while he was under a sink in a client’s kitchen in the North Valley.

“My phone buzzed with the bank alert and I literally stopped what I was doing,” he said. “I just sat there for a second on the tile floor. Then I texted my daughter in Denver.”

He paid the Bernalillo County Treasurer $4,800 in overdue property taxes that afternoon, including approximately $96 in accumulated late penalties — two months’ worth at 1% per month. The remaining $2,504 went toward his student loan servicer to bring his account current and make a small additional principal payment.

When I asked Byron what he would do differently, he paused for a long time. “I’d adjust my withholding so I’m not waiting on a big refund in the first place,” he said. “I’d rather owe a little in April than sit here for two months waiting to pay a bill that’s charging me interest.” He stopped himself. “But that’s easier to say now than it was to figure out before.”

That bitterness — tempered but present — defined every conversation I had with Byron. He is not a man who dwells, but he carries his financial setbacks with a kind of careful awareness, as if cataloguing them against future risk. Carmen’s death, the graduate degree pivot, the 2019 contract miscalculation, and now this. He knows the list by heart.

What struck me most, sitting across from him in that library, was not the size of his refund or the length of his wait. It was the precision with which he had planned around money the IRS had not yet confirmed sending. The system assumed everything would go smoothly. For Byron, this time, it did not — and the gap between assumption and reality cost him nearly $100 in penalties and two months of anxiety he could not afford.

(function(){var w=document.getElementById(‘pvv-scenario-s1775662814669fj5i’);if(!w)return;var btns=w.querySelectorAll(‘button[data-choice]’);btns.forEach(function(b){b.addEventListener(‘click’,function(){if(w.dataset.revealed)return;w.dataset.revealed=’1′;btns.forEach(function(x){x.style.opacity=x===b?’1′:’0.45′;x.style.cursor=’default’;x.style.transform=’none’});var o=document.getElementById(‘s1775662814669fj5i-out-‘+b.dataset.choice);if(o){o.style.display=’block’}});b.addEventListener(‘mouseenter’,function(){if(!w.dataset.revealed){b.style.borderColor=’#38bdf8′;b.style.transform=’translateX(4px)’}});b.addEventListener(‘mouseleave’,function(){if(!w.dataset.revealed){b.style.borderColor=’#334155′;b.style.transform=’none’}})})})();

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply