According to the IRS filing season statistics, more than 33 million American families claimed the Child Tax Credit on their 2025 federal returns — and a measurable share of those refunds were held pending identity verification, sometimes for weeks, sometimes for months. For most people, that delay is an inconvenience. For Daryl Rollins, a 47-year-old warehouse supervisor and single father from Birmingham, Alabama, 61 days felt like a lifetime.

I met Daryl in late March 2026, sitting in a pale-blue plastic chair in the waiting room of a Social Security Administration office on Lakeshore Parkway. I was there to report on a separate story about SSA appointment backlogs. Daryl was there to ask questions about his two-year-old daughter’s Social Security card after a paperwork mix-up. We got to talking. Within ten minutes, he was telling me about the IRS.

A Return That Should Have Been Simple

Daryl earns roughly $78,000 a year managing a 40-person warehouse team for a logistics company outside Birmingham. He is not a complicated tax case on paper. He files as head of household, claims one dependent — his daughter, Amara, born in January 2024 — and takes the standard deduction. He used TurboTax, same as the last four years.

He filed electronically on January 28, 2026. The IRS accepted the return the same day. Where’s My Refund, the IRS tracking tool, initially showed a projected deposit date of February 18. Daryl told me he had already mentally allocated the money: $1,500 toward a credit card balance carrying a 24.99% APR, $800 for a car repair he had been deferring since November, and the rest into a small savings buffer for Amara’s childcare costs.

On February 19, he checked Where’s My Refund. The status had changed from “Return Received” and “Refund Approved” back to a generic processing message — with no explanation. The projected deposit date had disappeared entirely.

What the IRS Letter Actually Said

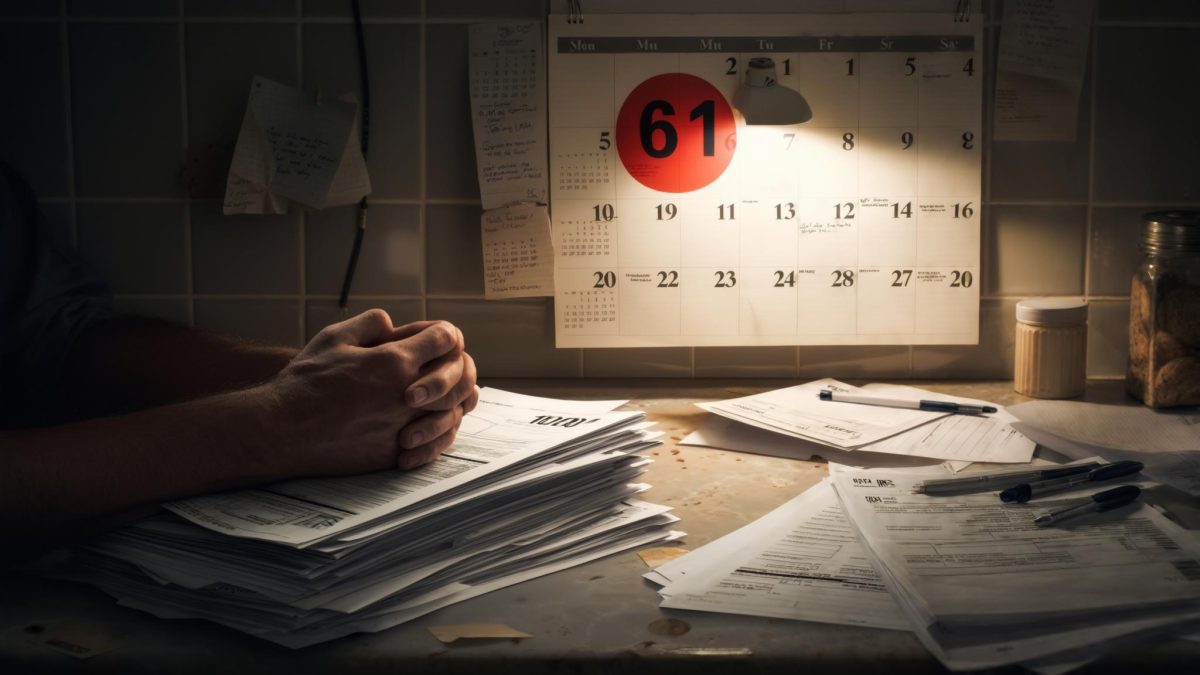

On February 24, Daryl received a CP05 notice in the mail. The CP05 is a standard IRS hold letter — it does not accuse the taxpayer of wrongdoing, but it does notify them that the IRS is reviewing their return to verify income, withholding, tax credits, and Social Security numbers before issuing a refund. The letter gave him no deadline and no specific reason for the review.

Daryl told me he read the letter three times. “I kept looking for the part that told me what I did wrong,” he said. “There was no such part. That almost made it worse.” He called the IRS taxpayer assistance line the following Monday. After a 47-minute hold, a representative confirmed the return was under review and told him to allow up to 60 days from the date of the letter before contacting the IRS again.

The Waiting, and What It Cost Him

The 60-day window the IRS representative cited turned Daryl’s carefully built plan into a waiting game. February became March. The car repair he had been deferring turned urgent — a cracked serpentine belt left him stranded on I-20 on a Wednesday morning, causing him to miss four hours of work. He paid $340 on a credit card he had been trying to pay down, not add to.

The childcare bill for March came in at $1,140. He covered it, but it meant pulling money from a small checking account cushion he had been building since Amara was born. “I’ve been trying to do better,” Daryl told me. “No retirement savings, credit score still recovering from some dumb stuff I did in my early 40s. This refund was supposed to be the first domino. And then it just sat there.”

Daryl is candid about his own patterns. He describes himself as someone who cycles between what he calls “hustle-mode” — long warehouse shifts, side jobs fixing cars on weekends, obsessive budgeting — and what he calls “panic-mode,” where anxiety drives impulsive spending. During the 61-day hold, the panic crept in. He bought a $220 baby monitor he did not need, “because it made me feel like I was doing something.” He acknowledges it without excusing it.

How the Hold Finally Resolved

On March 27, 2026 — 60 days after the CP05 notice date — Daryl checked Where’s My Refund again. The status had updated overnight: “Refund Approved.” A direct deposit date of March 30 appeared on the screen. No explanation, no second letter, no phone call from the IRS. The review had simply concluded.

The $4,200 hit his account on a Monday morning. He told me he sat in his truck in the warehouse parking lot before his shift and stared at the balance. “I cried a little,” he said. “Which I was not expecting.”

The Refund Arrived — and So Did Old Habits

Daryl paid the $1,500 credit card balance he had targeted. He paid the mechanic $340 he owed for the emergency belt repair — reimbursing himself, in a sense, for the unplanned expense. He set aside $600 for two months of additional childcare costs. That accounting puts him at $2,440 of the $4,200 spent on plan.

The remaining $1,760 is where the story gets complicated. Daryl put $500 into a savings account. He bought Amara a toddler bed and a set of books — roughly $380. Then, in what he describes with equal parts pride and frustration, he spent $880 on a used SmithCraft bass boat he had been eyeing on Facebook Marketplace for six weeks. “It was a steal,” he said. “I know that doesn’t sound like a financial strategy.”

When I spoke with Daryl on the day we met — March 31, 2026, the day after his deposit cleared — he was not sure whether to feel relieved or embarrassed about the boat. He landed somewhere in the middle. He knows he has no retirement savings at 47. He knows his credit score, which he tracked to 618 at the start of 2026, would benefit more from consistent paydown than from a bass boat registration fee. He said all of this without being prompted.

“I know exactly what I should have done,” he told me. “I just didn’t do all of it.” There is a particular kind of self-awareness in that sentence — the kind that does not quite translate to changed behavior, but does not pretend to be something it is not, either.

What Daryl’s Story Reflects About the 2026 Filing Season

CP05 notices are not rare. The IRS issued millions of them in recent filing seasons as part of broader identity theft and fraud prevention efforts, particularly for returns claiming refundable credits like the Child Tax Credit and the Earned Income Tax Credit. For taxpayers who file early — as Daryl did, on January 28 — the wait can feel especially dissonant. You did everything right, you filed on time, and then you wait longer than someone who filed in March.

Daryl’s situation also highlights a tension that does not get discussed much in personal finance coverage: high earners can carry the same structural vulnerabilities as lower-income filers when a single expected payment is delayed. His $78,000 salary looks comfortable in isolation. With a two-year-old, no co-parent contributing, a damaged credit profile driving up borrowing costs, and no retirement cushion, the monthly margins are thinner than the gross income figure suggests.

He is already thinking about next year’s filing. He has asked his employer to adjust his W-4 withholding so his refund will be smaller — closer to $1,500 — and his monthly take-home pay will be higher. “I don’t want to give the IRS a free loan and then stress out for two months waiting to get it back,” he said. It is a line I have heard from tax preparers for years. Coming from Daryl, it sounded newly earned.

When I left the SSA office that afternoon, Daryl was still waiting to speak with a representative about Amara’s Social Security card. He was on his phone, probably checking something. Maybe his bank account. Maybe Facebook Marketplace. Probably both.

Vivienne Marlowe Reyes is a Senior Tax & Stimulus Writer at Check Day America covering IRS payment timelines, refund delays, and the human stories behind federal tax policy.

Related: My Neighbor Got a $6,500 Tax Refund While I Got $400 — The Federal Tax Credits She Claimed That I Ignored

Related: She Counted on Her Tax Refund to Pay Rent. Then a Debt Collector Claimed It First.

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply